Company News

GTPL Hathway-Robust performance, ICICI Direct Research

GTPL Hathway (GTPL) reported a robust operating performance in Q4FY21. Revenues at ₹748.7 crore were down14.2% YoY. However, ex-EPC, revenues were at ₹ 560.1 crore, up 18.2% YoY, led by growth broadband and placement income. Subscription and broadband revenues were at ₹ 266.5 crore and ₹ 81.7 crore, respectively. Reported EBITDA increased 2.4% YoY to ₹ 116.4 crore. EBITDA margins at 15.5% were down 180 bps YoY post increase in operating expenses. Core EBITDA was up 1.5%YoYto ₹ 102.5 crore with margins at 18.3%, down 300 bps YoY. Subsequently, PAT was at ₹ 56.9 crore against net loss of ₹ 13.6 crore in Q4FY20.

Cable TV business stable; new market penetration key

Subscription revenues was flat YoY. Placement/carriage income jumped ~35% YoY at ₹ 179.7 crore, driving growth in the CATV business. On the subscription front, ARPU generated was at ₹ 122, marginally lower QoQ. Active subscribers(8 million) and paying subscribers (7.5 million) registered growth of 100K and 150K, respectively, compared to growth of 50K in Q3FY21. GTPL added 0.5 mn residential customers in FY21 and lost nearly same number of commercial customers due to the pandemic. The company maintained target of 50% growth in cable TV subscribers over the next three years on the back of expansion in newer markets and also through inorganic route. We build in ~6% subscription revenues CAGR in FY21-23E.The company will take a call on increase in pricing once normalcy returns.

Broadband segment grows again

Broadband segment reported stupendous growth of 77.2% YoY to ₹ 81.7 crore, driven by strong addition of 45Ksubscribers during the quarter and ARPU growth (up 5.5% YoY at ₹ 445). GTPL added 230K subscribers during FY21 leading to total ₹ 635K subscribers. The company incurred capex of ₹ 175crore in FY21 in the broadband segment and guided for ₹ 225-230 crore capex in FY22E. GTPL’s hybrid STBs are expected to be launched in Q1FY22E. We estimate healthy broadband revenue growth of 29% CAGR in FY21-23E, on a higher base.

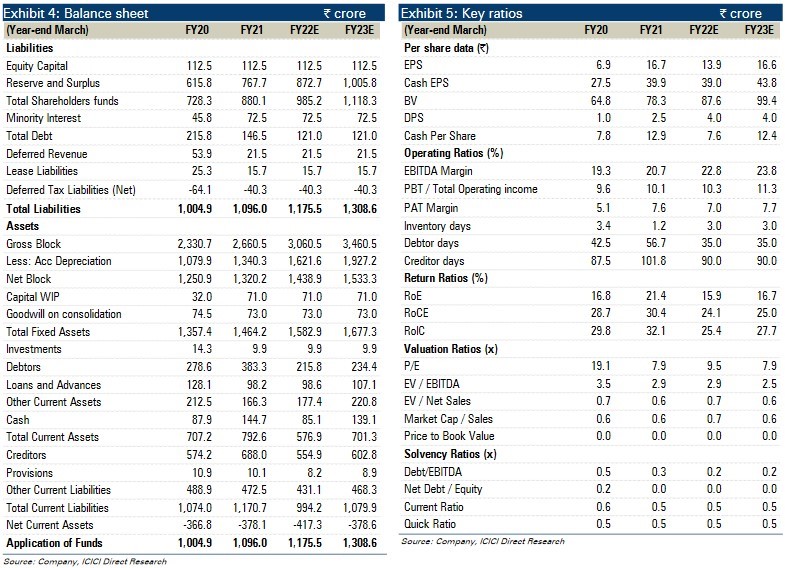

Valuation & Outlook

Valuation & Outlook

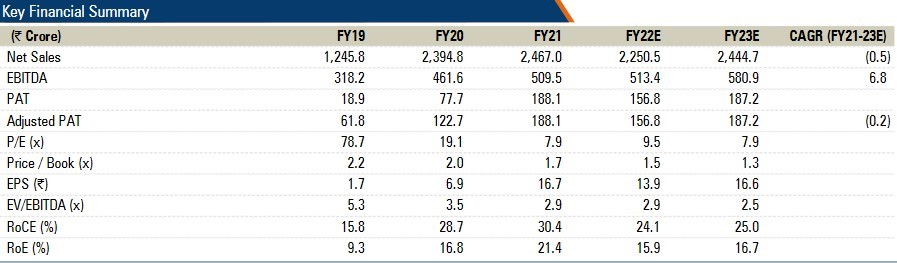

GTPL’s strong operating performance has been a result of remarkable growth in the broadband segment. We remain constructive on the company given the superior financial metrics with leadership in its key markets. The company has achieved net debt free status in FY21 and has declared dividend of ₹ 4/share in FY21. We revise our estimates slightly downwards post reduced activation income and management commentary on margins. We believe a strengthened balance sheet warrants higher valuations and raise our target multiple. We maintain BUY rating with a revised target price of ₹ 165/share (previous TP: ₹ 175) at 10x FY23E EPS.

Conference Call and business highlights

Conference Call and business highlights

- FY21 performance: Subscription revenue was up 3.9% YoY while broadband revenue jumped 66.8% YoY. Consolidated revenues increased 3% YoY while ex-EPC revenues increased 18.5% YoY. Cable TV active subscribers were at 8 mn, flat YoY. Broadband active subscribers were at 635K (addition of 230K YoY) with ARPU at ₹ 440 (4.3% growth YoY)

- Hybrid box expected launch in May: The management said launch of hybrid box (single package including cable, broadband and OTT services) is expected in May. The management declined to share the details regarding pricing, launch strategy, etc, and said it will disclose the same at the time of the launch

- Broadband, cable growth guidance: The management expects strong addition of broadband subscribers (~50K per quarter) to continue, going forward. In the CATV segment, the management is targeting 50% growth in subscribers over the next three years. CATV expansion will be via both organic and inorganic route. The management said the company added 0.5 mn residential customers in FY21 and lost nearly same number of commercial customers due to the pandemic

- Capex guidance increased; CATV ARPU stable: GTPL incurred a capex of ₹ 335 crore in FY21 (₹ 175 crore in broadband and ₹ 160 crore in CATV). It has increased capex guidance to ₹ 400 crore for FY22E. Broadband capex is expected to be ₹ 225-230 crore while the rest will be deployed towards the CATV segment. Cable ARPU was at ₹ 122 during the quarter while broadband ARPU was ₹ 445. The company will take a call on increase in CATV pricing and overall package restructuring once normalcy returns. Broadband ARPU is expected to increase 5% in FY22E. A provision for insurance claim of ₹ 3.3 crore in broadband was made during the quarter

- EPC project nearly completed; O&M revenue to continue: GTPL has booked ₹ 1038 crore EPC revenue out of total ₹ 1073 crore till the end of FY21. The company has booked ₹ 27.4 crore O&M revenue in FY21 while ₹ 57 crore annual revenue is expected in the next seven years with 20% margin

- Activation revenue dips; one-off revenue/costs from merger: Activation revenues declined due to a dip in deferred revenue. Reduction in activation revenue slightly affected EBITDA margin. The management said activation revenue is expected to stabilise from FY23 onwards while margins are also expected to increase. GTPL reported ₹ 23.9 crore revenue from merger of subsidiaries leading to higher other income with similar amount charged in costs

- EPC payment expected in May; marketing spends for launch of new products: Total receivables were at ₹ 383.3 crore with cash & cash equivalents at ₹ 144.7 crore. Receivables breakup: placement & activation income -₹ 110 crore, EPC-₹ 226 crore. The management expects ₹ 200 crore EPC payment by May. The company said 0.5% of revenue will be utilised towards marketing budget

- Other highlights

- Out of 3.87 million broadband home pass, 65% home pass is available for FTTx conversion. Data consumption per customer was 212 GB/month as on end of March 2021, up 31% YoY

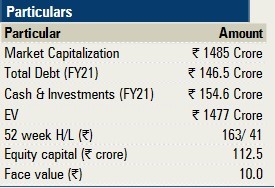

- While gross debt was at 146.5crore, the company became net debt free in FY21

- The management does not expect any major impact of possible lockdown

Money Control

Money Control

You must be logged in to post a comment Login