BCS Stories

OTT is changing the television experience

Over the past two decades, there has been a monumental shift in how people access and consume video content. With the universal access to broadband internet, numerous platforms like YouTube, Netflix, Prime Video, Disney+ Hotstar emerged and steadily grew to prominence. These platforms became successful by catering to media-hungry audiences and fitting around their increasingly hectic lifestyles.

The ages-old TV-watching experience is no longer limited to real-time nor the TV screen in the living room. Content is now consumed on laptops, tablets, handheld devices, game consoles – whenever and wherever people like. Although not a household name in itself, OTT is the exact technology that made the streaming revolution possible.

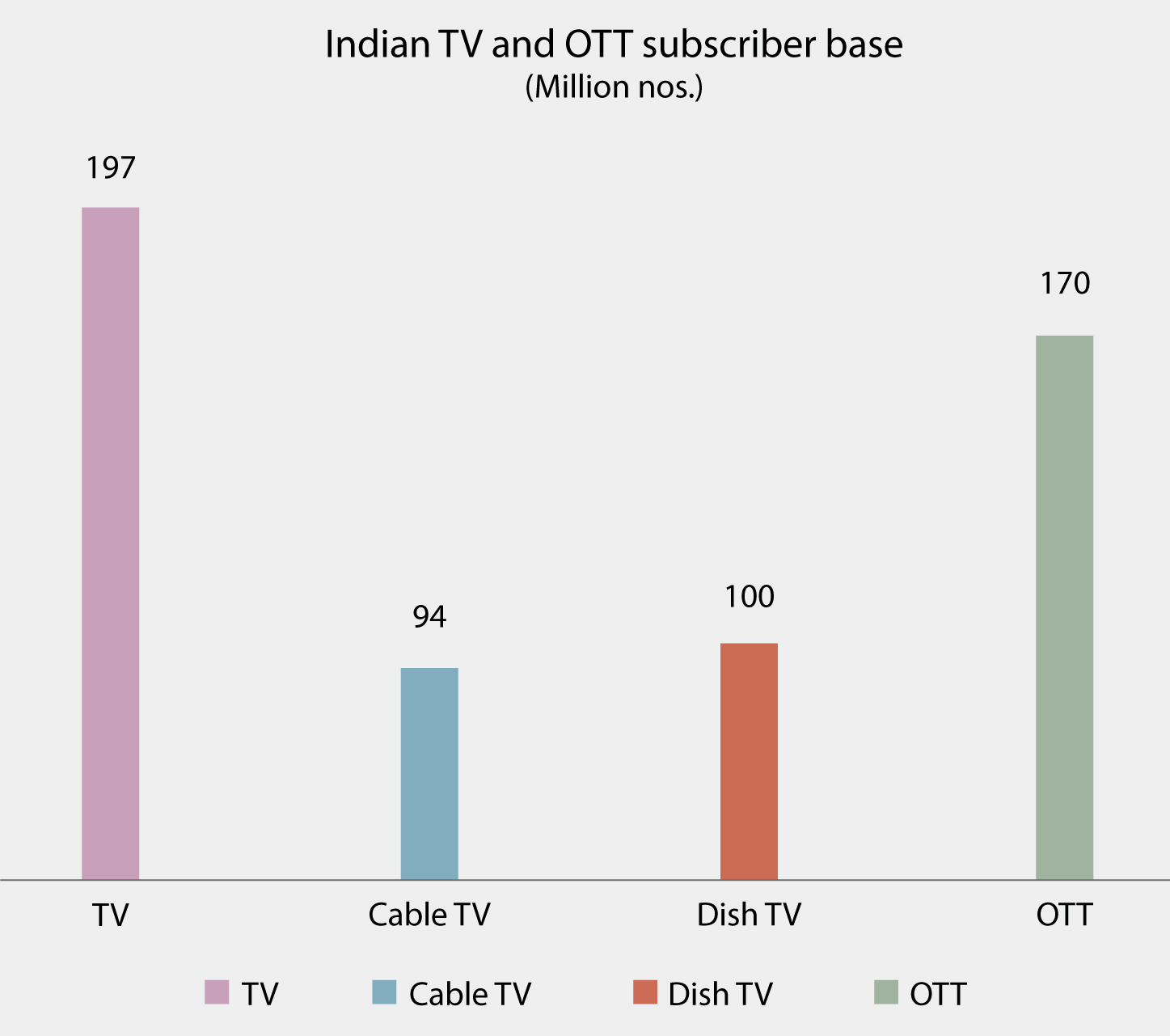

2020 was the year of OTT, with consumers seeking out digital entertainment in the stay-at-home ecosystem and the new normal is going to continue to drive demand. In fact, 2020 has seen subscriptions to OTT services surpass pay TV, with the trend likely to continue, as OTT subscriptions are expected to rise further by 7.71 percent during 2021. Disney+ aimed for 90 million subscribers by 2024, and managed to meet that target in just 8 months. New services are hoping for similar success, including CBS All Access (Paramount+), Discovery+, and Peacock from NBC Universal.

India’s OTT market continues growth

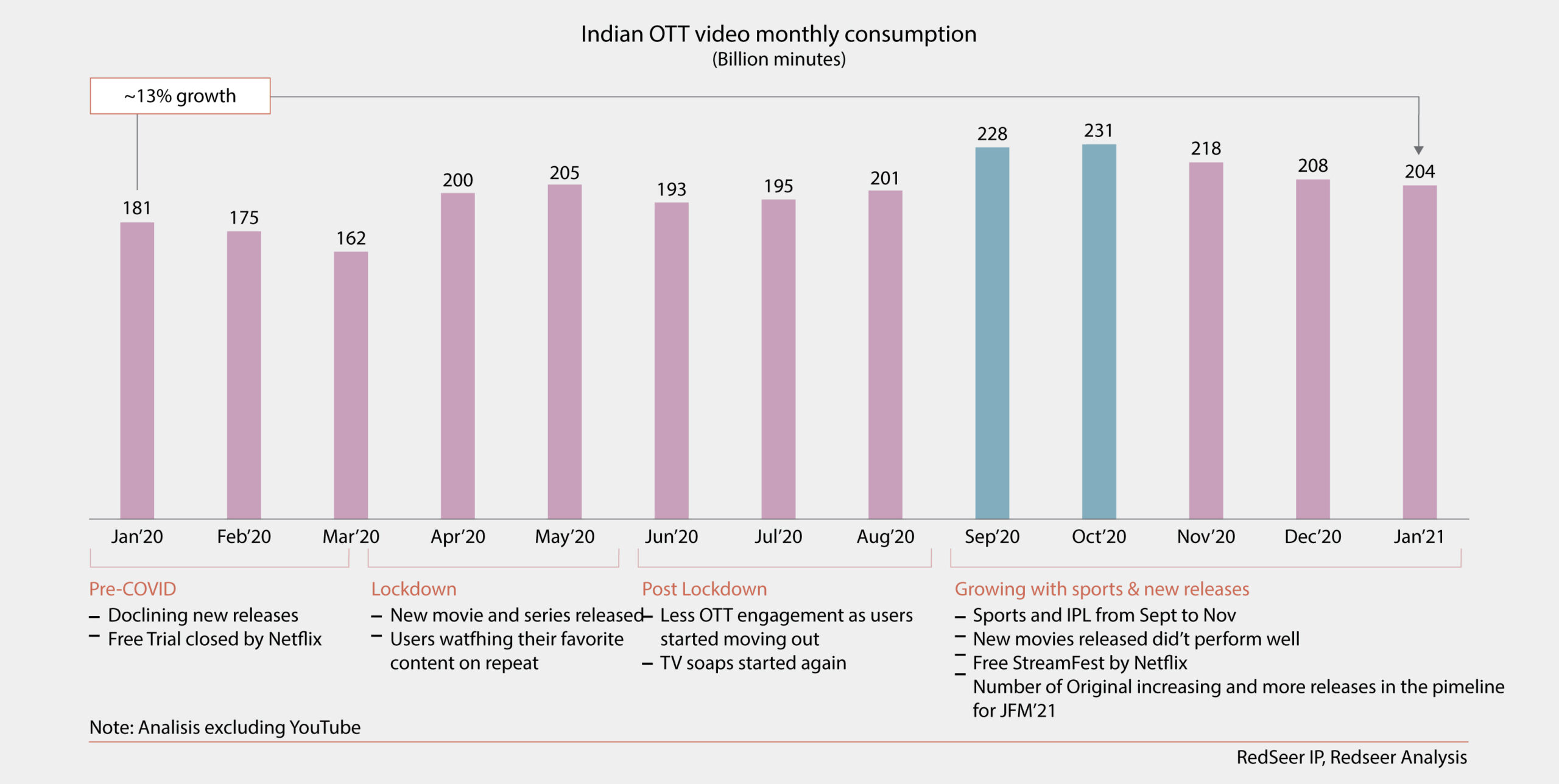

India’s OTT market remains one of the fastest growing markets in the world. Over the past 12 months, spurred on by the COVID-19-induced lockdown, total domestic OTT consumption increased from 181 billion minutes to 204 billion minutes.

Monthly OTT consumption, however, showed significant variation over the 12 months, according to RedSeer. The differences not surprisingly followed the pattern of the lockdowns imposed by the government, dipping to 195 billion minutes of OTT consumption in June, and then jumping to 231 billion minutes in October. Fourth quarter consumption was also lifted by a number of major OTT releases, including sporting events, new movies and a campaign from Netflix to ramp up its following in India.

According to a Boston Consulting Group report from two years ago, India’s OTT market is poised to reach USD 5 billion in size by 2023, although this number should likely to be revised upward on the back of the rapid uptake seen during COVID-19.

The first dependent OTT platform in India was BIGFlix, launched by Reliance Entertainment in 2008, however, today US giants Netflix and Amazon Prime Video are among the largest players. In terms of customer satisfaction, the SVoD platforms Netflix and Amazon Prime Video also lead the way with scores of over 50 percent, meaning that a majority of users would recommend buying the streaming service to peers. However, in terms of the number of subscriptions, Hotstar (now Disney+Hotstar) is the most subscribed to OTT platform in India, with around 300 million active users and over 350 million downloads.

At present, the subscribers are evenly spread between the metros and rest of the markets, and the future would be driven by the non-metros, semi urban, and rural markets. With the boom in almost every consumer-based industry, players here have understood the importance of personalizing and catering to the consumer base in Tier-II and Tier-III cities of India. It has become a matter of growing importance to understand how to enter these markets as these segments have different user behaviors as compared to the metropolitans in India.

Global scenario

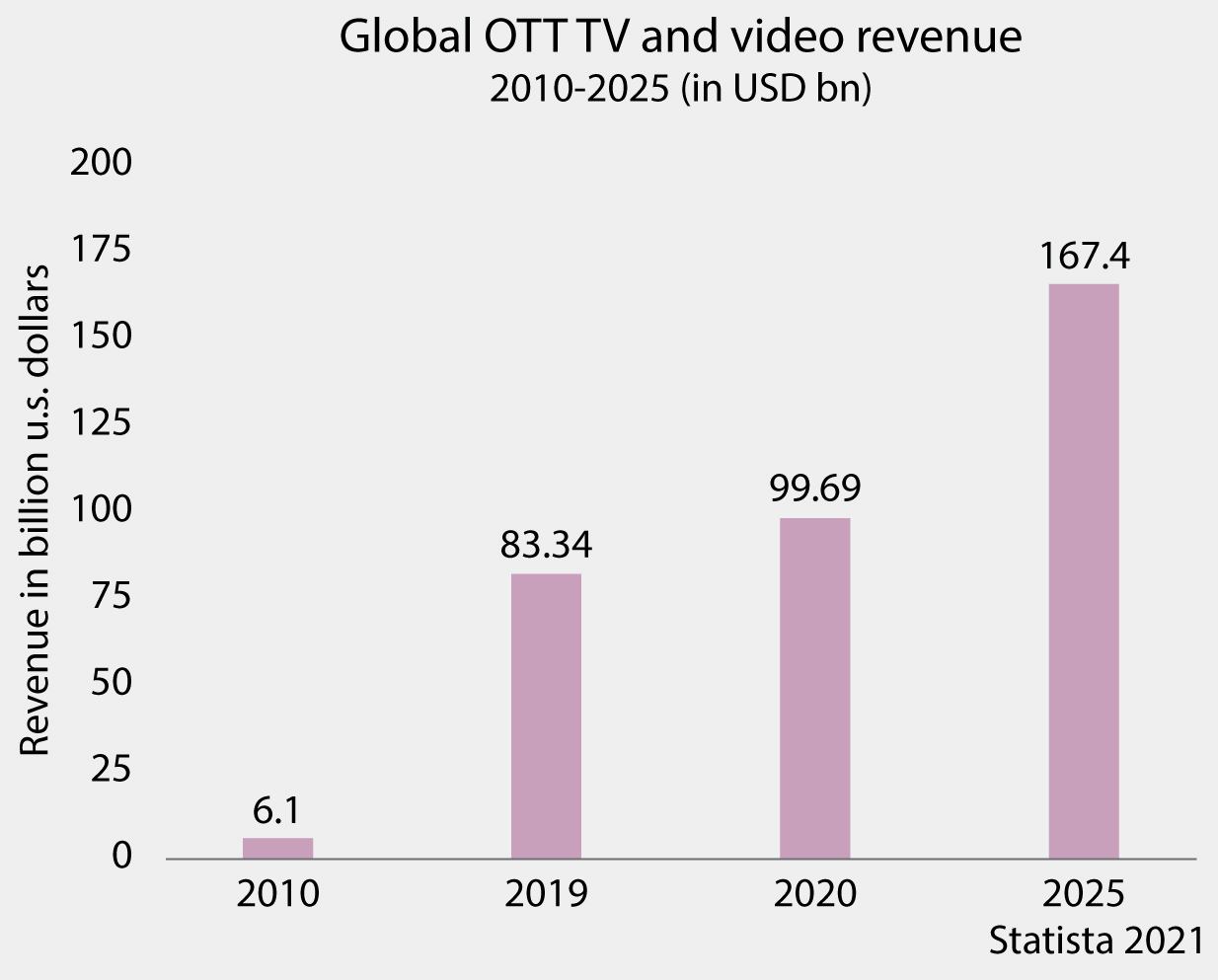

The global OTT media revenue is expected to reach over USD 167 billion by 2025, more than double the 83.3 billion generated in 2019. The primary engine for this growth will be from traditional broadcasters increasingly turning to streaming services in order to extend their reach and compete with online video giants.

Surprisingly, the biggest subscription streaming platform in the world actually saw its global market share decrease from 29 percent to 20 percent, an overall decline of 31 percent, with a flurry of new competitors, entering the SVOD market. With the emergences of new subscription services, other incumbents saw drops in market share, too, in 2020. Amazon Prime Video saw its market share decline from 23 percent to 16 percent, according to Ampere.

As subscription services become increasingly prominent, different models will be needed to combat subscription fatigue, according to Juniper Research. In 2020 there was an average of four SVoD subscriptions per household in the US, but with growth slowing significantly from 2021.

One successful model is the hybrid service, a combination of subscription- and advertising-supported monetization, such as NBC’s Peacock, and CBS All Access, which offer tiered services that still generate subscription revenue but show advertisements in lower-priced bands in order to keep end user prices down. Juniper Research anticipates that these services will account for $1.4 billion in advertising spend in 2025.

Thanks to this high level of market saturation, streaming providers need to keep their offerings competitive to retain subscribers. Hybrid monetization is one way that VoD providers can keep their offerings low-cost, and therefore less likely to be dropped.

Are we hitting subscription saturation point?

The subscription model is everywhere and extends far beyond the boundaries of OTT streaming. Wallets do not, and consumers are being faced with budget decisions on everything from TV to homewares. In 2020, the consideration of how many subscriptions were too many was a hot topic, and still is. The Big Three – Netflix, Amazon Prime Video and Hotstar, have seen their growth slow, as Disney+ reclaims rights to its content, and consumers find their favorite shows now spread across multiple platforms. As other studios and rights holders aim to seek to launch their own services, how many services will customers be willing to purchase?

Aggregation on the horizon

With the prospect of OTT fatigue discouraging customers to subscribe to new services, broadcasters will need to start working together to aggregate services. The BBC and ITV in the UK have Britbox. Germany’s Joyn started off as a standalone streaming service before partnering with Discovery, as well as supporting a number of other German channels. Smaller studios and vendors, unable to match the subscription numbers of Amazon and the growth of Disney+, are likely to move toward a more co-operative approach.

Another emerging trend likely to continue is the bundling of OTT and SVoD subscriptions with other services. Google also appears to be working on an aggregator app built into Chrome, called Kaleidoscope, though there are no guarantees this project will become widely available to users, which is thought to support Netflix, Amazon and Disney+Hotstar as an authentication aggregator rather than a direct partnership between the three services.

As more and more OTT services enter the market, and rights move around, demand for aggregators will increase as consumers try to work out which services are right for them. There’s a definite gap between entertainment news sites, and aggregators, that would guide consumers to create the right DIY bundle of services for their needs.

So, while a single aggregator that grants access to the major OTT platforms is unlikely in the short term, the threat of competitors banding together to take their crown might force a change of strategy further down the line.

4K will become the standard proliferation

Twenty-one percent of all TVs in use are estimated to be 4K in 2020, compared to just 0.01 percent of smartphones/tablets. Lower resolution content will continue to be the standard for mobile for a while, whereas 4K will overtake HD as the standard for TV. OTT services have a clear technical advantage cable/STB services in serving this need, which will further drive the shift toward OTT and opening additional opportunities. 2020 has already been the worst year on record for pay TV cord cutters, with eMarketer reporting that by 2024, more than a third of US homes will have cancelled their pay TV services, bringing the total of cord cutters to 46.6 million. The trend is a 7.5 percent drop YoY, which is presenting huge opportunities for OTT services with the right content offered at 4K streaming resolution.

2021 could be the year of PVoD

Premium video on demand (PVoD) – the delivery of content outside of the typical subscription offering and traditionally sports-led – is a growing market, with 22 percent of US streaming customers paying to watch a direct-to-service movie in 2020 due to the closure of cinemas globally. Universal Pictures have seen success from releasing movies directly to digital. However, with more than 60 percent of millennial and Gen X viewers reported to be willing to watch a film in the cinema in the next 6 months, widespread PVoD services are more likely to become a competitor to, rather than a replacement of, the cinema experience.

Ad spend will surge on streaming video

Marketers across the board are gearing up for a big push in 2021, and ads in streaming video are a huge market. Following a 6.9 percent decline in digital ad spend in 2020, the prediction is that this will jump to 20 percent in the coming year. With the predicted shift from pay TV to streaming previously mentioned, advertising is following the trend. Those households that are cutting the cord are opting for DIY bundling, opting for a combination of premium and specialized SVoD and several AVoD services. This gives the opportunity for advertisers to target demographics based on the audiences of these services and focus their spend. OTT providers may find that identifying and specializing to these markets can increase ad investments as a result.

Consumers have more choice than ever before, which could drive churn

Parks Associates reported that churn in streaming services rose to 41 percent during the first quarter of 2020 from 35 percent in the same period of 2019. Content fragments across services, rights are transferred, new shows for SVoD services go exclusive, sports rights are divided between services, and original content is exclusive. All these factors contribute to subscribers with itchy trigger fingers, ready to churn and move to the next service. Of course, this could also mean the same customers come back for their favorite shows, but it will become more and more difficult for major SVoD services to retain their customers for long periods of time. Specialized, niche services may find that customers can be retained more easily by service their niche, but all providers will need to ensure they can move quickly to re-engage customers when a competitor launches content that is likely to be in high demand.

Outlook

With the outbreak of COVID-19 various lockdown policies around the world, OTT has become one of the few remaining – but much-needed – sources of entertainment these days. This explains its explosive growth in the recent years – the effect is very likely compounded by the cord-cutting trends and a gradual switch to online-only media consumption. For advertisers, OTT services will soon be the only way to reach some TV audiences which do not use regular TV, cable, or IPTV.

2021 is not going to be the back to normal year; even at best estimates, the first half will likely mirror 2020 in terms of consumer habits. The OTT environment will change substantially as providers have had almost a year’s opportunity to read the crowd, adapt, develop, and release new methods of reaching their audience.

Churn will be a major challenge. The fragmentation of content across more OTT services alone will mean customers will be basing their subscription choices on their favorite content and will happily churn and re-subscribe as they move between services month-by-month. Retaining customer loyalty will require great data analysis, serving the right content at the right price.

You must be logged in to post a comment Login