Reports

The era of consumer ART

Indian media companies will be constantly challenged on what they should prioritize in the horizontal world — how to acquire customers, strategies to engage them, new models of monetization, which technologies to adopt, how to get audiences to create content, how to manage communities, and how to transform through all these aspects in an agile manner.

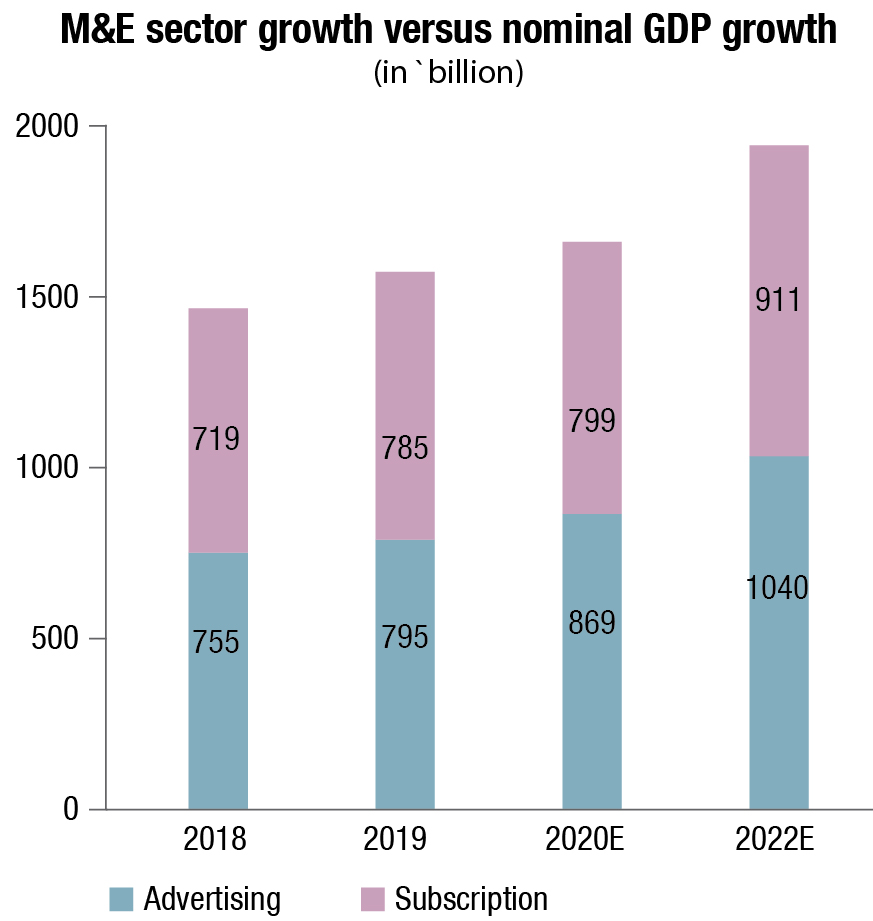

The Indian media and entertainment (M&E) sector touched ₹182,000 crore, a growth of 9 percent over 2018. It is expected to reach ₹242,000 crore by 2022 at a CAGR of 10 percent. Digital media overtook filmed entertainment in 2019 to become the third-largest segment of the M&E sector; it is expected to overtake print by 2021. The 2020 estimates were created prior to the advent of coronavirus (COVID-19).

Key trends in 2019

Digital advertising aggregated the largest share of marketers’ incremental and performance-driven advertising investments, growing 24 percent in 2019 to command the highest-ever share of 24 percent of total advertising revenues, up from 20 percent in 2018. Digital subscription grew over 100 percent in 2019 as sports and quality video content went behind a paywall and telcos paid more to bundle content with their data packs; it now comprises 13 percent of total digital-segment revenues. TV advertising saw 5 percent growth in 2019 owing to large-impact properties like the ICC World Cup and the general elections, while subscription grew 7.5 percent due to increase in the end-customer prices.

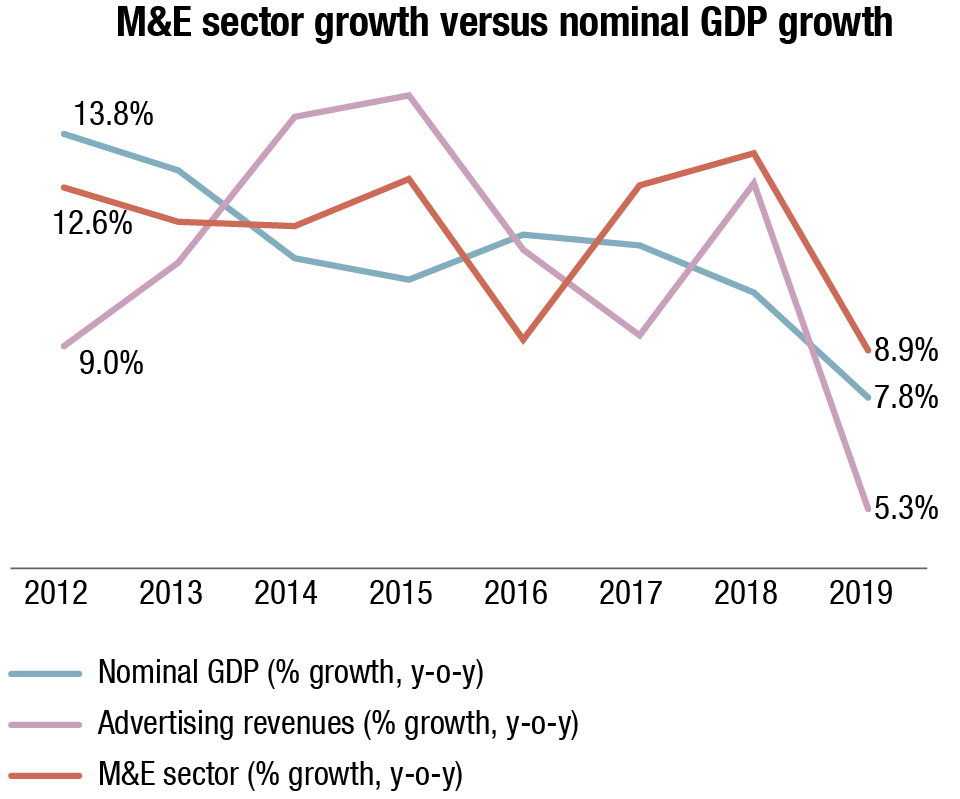

M&E sector outperformed the Indian economy. India’s nominal GDP grew at 7.8 percent in 2019, an 8-year low in growth terms. Advertising, correspondingly, grew at just 5.3 percent though the M&E sector grew at a higher rate than the economy, demonstrating the relative power of subscription-based business models and India’s attractiveness as a content-production and post-production destination.

2019 saw robust M&E deal activity. There were 64 deals in 2019 compared to 41 deals in 2018, yet the overall deal value was much lower at ₹10,100 crore as compared to ₹19,200 crore in the previous year. Eighty-four percent of deals were in the new media space while just 16 percent of deals were for traditional media. Private equity and venture capital provided over 60 percent of funding.

Subscription outpaced advertising growth. Advertising grew 5.3 percent while subscription grew 9.3 percent in 2019. Advertising growth was muted due to overall economic slowdown in 2H19, which also impacted festive ad spending and resulted in a polarization of spends toward impact properties. The net increase of ₹4000 crore in ad spends was because of ₹3700 crore growth in digital and ₹1500 crore growth in TV, reduced by a fall of ₹1200 crore across local traditional media (print, radio, OOH). Subscription growth was driven by OTT video consumption (111%), film (10%), and TV (7.5%). Advertising is expected to grow at a 9-percent CAGR over the next 3 years.

SME digital-advertising market grew 25 percent. The small and medium enterprises (SMEs) comprise over 45 percent of omg India’s industrial output and 40 percent of India’s exports. SMEs are estimated to spend around ₹8750 crore on digital advertising, primarily on search, social, and e-commerce platforms. SME advertisers on digital number over 350,000 and are predominantly focused on regional, performance advertising.

Digital subscription continued its robust growth trajectory. Streaming-video revenues grew over 100 percent from 2018 as sports and premium content went behind the paywall, leading platforms launched sachet-priced packages, and the number of consumers consuming content on telco bundles crossed 260 million. Audio-streaming revenues grew as well, though the growth was relatively muted at 18 percent. Many newspaper companies put digital versions of their print products behind a paywall, though monetization of the same remained nascent.

NTO changed television as viewers knew it. The New Tariff Order (NTO) implemented during February 2019 increased the end-customer prices for TV content, reduced the reach of certain genres of channels, and resulted in a 6 percent reduction in time spent watching TV during 2H19. While subscription revenues increased in 2019, certain customer categories ended up cutting the cord and moving to digital, while others reduced spends or switched-off their second and third TV sets in the home. Free-TV grew in 2019. Unidirectional TV (pay+free) is estimated to reach 171 million households and that there were over four million connected-smart-TVs at the end of 2019.

Outlook

Growth in video consumption will provide opportunity across all customer segments. From around 550 million TV and smartphone consumers currently, a billion screens are expected by 2025, of which 250 million screens would be TV-sized while 750 million would be smartphones. This could result in a continued growth in demand for content – both long-form episodic and short form – as well as provide significant opportunities for content creators and UGC platforms. Connected-TV sets are expected to grow to around 40 million to 50 million by 2025, from around 4 million sets currently, on the back of increased wireless and wired broadband connections and proliferation of low-cost smart TV sets. This will provide an opportunity to existing and new content creators to produce content for these screens, and reach customers directly, without passing through aggregators. The unified interface on TV sets or STBs will be of prime importance for content discovery, marketing, and customer experience. Traditional media will embrace platformmatic advertising sales.

COVID-19 to impact India’s economy

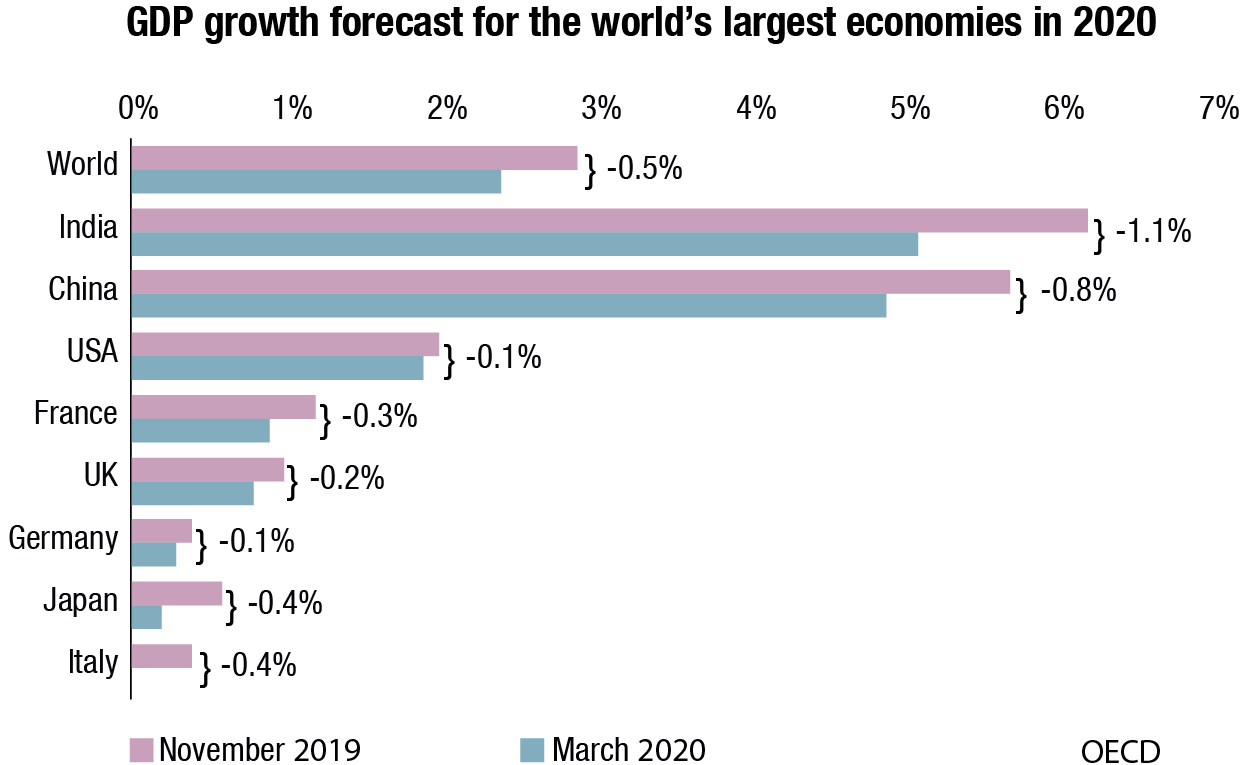

While it is too early to gauge the economic impact of the COVID-19 outbreak, the Organisation for Economic Co-operation and Development (OECD) reduced its growth forecast for India by 1.1 percent for 2020, though still showing India as the fastest-growing major economy in the world. This could impact the advertising revenues forecasted for 2020. The impact on various segments of M&E could include postponement/cancellation of events, impact on theatrical revenues due to loss of weekends, stoppage of print production/circulation in impacted areas, newsprint import blockage, and stoppage/delay of content production and post production. Positives could include increased time spent with media in the home.

Segment trends – Television

TV advertising grew by 5 percent in 2019, mainly on the back of sports, marquee events, and general elections for news channels. TV AdEx volumes fell 4 percent in 2019, though five of the top 10 ad sectors grew their ad insertions. Advertising volumes grew 4 percent on regional channels. Subscription growth of 7.5 percent was mainly driven by a growth in the end-customer pricing on account of the implementation of the NTO in February 2019, while the number of active pay-TV subscriptions fell. Overall time spent on TV reduced 6 percent post the NTO (July–December 2018 vs.

2019). If strictly implemented, NTO 2.0 could reduce subscription income in 2020. The number of channels grew by 33 in 2019. Sixty-three percent of channels were free-to-air. MSO registrations increased by 11 percent during 2019. While large broadcasters’ extremely popular catch-up GEC and film channels were removed during the year, FreeDish’s channel strength increased by 24 during 2019.

Advertising

TV advertising grew by 5 percent. Increases were led by sports and marquee properties. TV advertising grew well in 1H19 on the back of sports and the general elections but witnessed de-growth in 2H20 at ₹32,000 crore, up 5 percent from 2018. Clear polarization was witnessed as marquee properties and sports saw interest continue to increase, while other genres saw stagnant or even falling interest. As per TAM AdEX, ad volumes fell 4 percent in 2019. The main fall was witnessed in 4Q19. The fall in reach due to implementation of the NTO also impacted ad volumes in February and March 2019. In addition, large broadcasters pulled out their GEC and film channels from FreeDish and made many of them pay-channels, which also impacted ad volumes.

Impact of NTO on advertising. There was no impact on total ad volumes (+0.2%) due to the implementation of the NTO. Regional channels grew ad volumes by 4 percent while national channels witnessed a 6-percent fall in ad volumes. Channel genres most positively impacted by the NTO included DTH home channels (+168%), Bhojpuri movies (+60%), Kannada movies (+58%), Punjabi music (+33%), and sports (+26%). Channel genres most negatively impacted were religious channels (–60%), English entertainment (–50%), English movies (–37%), and lifestyle (–36%) with the assumption being that English and lifestyle audiences moved away to relatively more affordable OTT products. While broadcasters cater to around 10,000 advertisers, digital web publishers cater to around 25,000 advertisers, and e-commerce platforms are estimated to reach over 300,000 SME advertisers.

Distribution

Total subscription paid for TV in India by viewers increased 7.5 percent in 2019, despite a fall in active paid subscriptions, on account of higher ARPUs. The subscription-base for traditional unidirectional television services is expected to keep growing as penetration levels increase over the next few years. Strict implementation of the NTO 2.0 from March 2020 could, however, result in an up to 4 percent fall in subscription income at end-customer prices in 2020.

But there would be a marginal growth of up to 2 percent in the event that bouquet size, pricing, and channel mix change. There has been growth both at the top end and bottom of the TV viewer pyramid. Substantial growth took place in smart TV set sales due to price reductions; industry discussions indicate four to five million connected-smart-TVs in India, up from less than two million in 2018.

Connected-smart-TV sets are expected to reach 14 million by 2022. On the other hand, FreeDish continued to grow and has become a second STB within the home, used when there are no large events on TV in some cases. End-customer prices are estimated to grow by over 25 percent on average to cross ₹225 net of taxes. While packs were created by DPOs combining channels from different broadcasters, there was little scope for discounting. Industry discussions indicate that over 85 percent of subscribers opted for DPO-designed packages, but slowly this number is reducing as subscribers start to opt for channels they require and let go of channels they do not watch. DPOs implemented different strategies for the NCF for additional TV subscriptions, with some charging it at full price while others provided a discounted rate.

The viewership of HD channels increased by 56 percent post NTO as compared to the pre-NTO period viewership.

Broadcaster share of revenues grew 10-15 percent owing to increased number of pay-channels, higher ARPU, and increased share of revenues from end-customers. The broadcasters’ share of total subscription income increased to approximately ₹13,000 crore. The HITS platform has commenced being used as a white-labeled TV distribution service. This is akin to the tower companies in the telecom sector and can result in significant benefits including reducing capital expenditure and operational savings due to scale.

Outlook

While pay-TV will continue to grow, more new users will enter the free-TV market, providing a low-cost advertising opportunity to marketers. Growth of unidirectional TV will be far outstripped by the growth of connected-TVs, which could cross 40 million connected sets by 2025, on the back of increased demand for HD content, replacement of obsolete STBs in 46 cities, which already have a population of over a million each and a total population of 122 million that can be wired up more easily for broadband. This will mean that overall TV will keep growing at a healthy pace of over 4 percent per year to cross 70 percent of Indian households by 2025.

Content viewed on smart TV sets will begin to reflect that consumed on mobile phones, providing a window for user-generated content companies and other non-broadcasters to serve content on the connected-TV screen. As more and more TV sets get connected to the internet, content will flow from creator to viewer and back, and more interactive concepts will emerge as king of advertising, even in 2025. TV is expected to remain the largest earner of advertising revenues even in 2025, approaching ₹57,000 crore.

The need for a common and accepted measurement metric to help marketers invest across digital and TV is required, and it will enable enhanced monetization of both traditional and digital-video inventory. Programmatic advertising would result in platform-led purchasing of video inventory and drive up to 25 percent of ad volumes by 2025. Viewership of regional language channels will continue to grow and reach 55 percent of total viewership in India as their content quality improves further.

The consumer ART

The era of consumer ART – acquisition, retention and transaction – is defined by a segment-agnostic media landscape, focus on D2C products, and differential techniques for acquiring, retaining, and transacting/monetizing the D2C relationship. Media was always verticalized in terms of segments (TV, radio, print, film, digital) with each producing content, editing, packaging, and distributing with distinct ecosystems. In a digitized world, the media of today is defined by five horizontal (i.e., segment-agnostic) sections – content producer or IP owner, aggregator, distributor, platform, and device. This segment-agnostic landscape has, hence, forced traditional media companies to redefine themselves into one or multiple of these sections. For example, many traditional broadcasters in the new media landscape are redefining themselves as content producers, while some are aggregating and yet others are placing their bet on building end-consumer platforms. Newspaper companies are creating audio and video content, building digital destinations, and serving more needs of their communities through transactions and classifieds. Content production houses have launched D2C platforms and invested in theatrical distribution. Telcos have launched D2C platforms and invested in content production.

In a digitized world, every media segment can directly connect with the consumer and stronger the direct relationship, the better the engagement and monetization. Hence, in the horizontal media landscape, greater value is attributed to D2C relationships, and D2C has emerged as the new metric to evaluate a media company. B2B businesses have hence gone B2C, and D2C relationships are dominated by new media and non-media companies. Therefore, to successfully build D2C relationships and stay at the top, media companies must learn the art of how to acquire, retain, and transact with the consumer.

While different companies are in different stages of this evolution, most large broadcasters and print companies have begun to build D2C relationships by ensuring that they have access to end-customer data. Digital media companies are slowly transitioning to the retain-phase to engage better with their acquired consumers through interactivity and premium services. Gaming and social-media services, on the other hand, have evolved well into the transact-phase with multiple monetization models for their already-acquired and engaged D2C relationships.

Consumer ART in M&E value chain

The era of consumer ART has redefined the media value-chain, leading to the emergence of many new trends and strategies across content, distribution, consumption, and monetization. Certain highlighted key strategies are:

ART of content. Media companies are today challenged to find techniques to produce transient yet engaging content and perform that consistently to acquire consumers with reduced attention spans. Many short-video services have addressed this challenge by encouraging the consumer to be the producer. The consumer is the new content creator and the creator community, hence, is the greatest asset of the platform. The community not only produces content but also acts as influencers whom advertisers tap into. This has led to increased advertising at low content costs. Media companies now face the challenge of building, sustaining, incentivizing, and growing such creator communities. The consumer no longer wants to just consume content passively but wants to participate, indulge, or be at the center of the experience. This will only be accentuated with the growth of immersive technologies like AR and VR. The consequence of a segment-agnostic media landscape is that the M&E sector can be re-imagined as per content formats and how they are progressing to immersive. The sector has moved toward text, audio, video, and experiential products.

ART of distribution. D2C relationships need new skills to market the service to the consumer, get them to download apps, share personal data, consume content, bill for the service, and keep them from churning away. In a traditional media ecosystem, these skills mostly rested with the distributor. Partnerships and collaborations are a key piece of the art, which media companies need to develop and learn to work through, rather than work with. Collaboration will be critical for success in future. Media services are bundled with payment wallets, taxi services, telco bundles, TV subscriptions, and e-commerce platforms. Media services earn syndication income from many of these aggregator apps but often do not get end-customer data. This trade-off between revenue and depth of data is a difficult balance between scale and value creation. Building D2C relationships in a bundled ecosystem is a new art form which media companies need to develop.

ART of consumption and monetization. From broadcasting a few pieces of content to millions of people to narrow-casting many pieces of content to niche audiences to unicasting millions of pieces of content tailored to one unique consumer, media has come a long way. Media companies, which are used to mass consumption, are learning the art of individual consumption, relying heavily on technology for the same. Technology is now a core part of any media operation and its importance will continue to grow. The art of determining the right mix of technology while retaining the human creativity will decide success for many media companies. Media services are now differentiated by whether they are advertisement driven, subscription driven, micro-transaction driven, or e-commerce driven. Each monetization model is enabled by a set of tools, some of which are acquisition, retention, advertising, subscription, and transaction. These tools are mere instruments and the subtle art of using them in an integrated manner will help to effectively monetize the consumer relationship. More than ever, particularly for ad-supported offerings, the need for a single-customer view has emerged.

Sale of space and sponsorships is moving toward performance-led advertising, irrespective of where the consumer is spending time, so long as the message reaches the desired audience. This will result in the need for unified measurement of media consumption (not just viewership) across video, audio, text, and experiential. Technologies like passive listening, deeplinks, image recognition, geo-tagging, and big data will come together to provide solutions to increase advertising efficiency.

Outlook

In the initial digital years, media companies were valued on customer acquisition with active users being key metrics. As they further evolved, customer engagement and retention became more valued with engagement depth being key metrics.

Indian media companies will be constantly challenged on what they should prioritize in the horizontal world – how to acquire customers, strategies to engage them, new models of monetization, which technologies to adopt, how to get audiences to create content, how to manage communities, and how to transform through all these aspects in an agile manner. Answers to these questions in the backdrop of a segment-agnostic media landscape leading to D2C relationships will define the new era and the next decade.

Based on The era of consumer ART – Acquisition | Retention | Transaction, a report by FICCI & EY India

You must be logged in to post a comment Login